GIGMETAR REPORT OCTOBER 2023

After the gig workforce registered substantial double-digit growth in the aftermath of the pandemic, the latest measurements reveal a major decline, of as much as 17.8 percent, in Serbian gig workers on the leading platform. This development has marked the reversal of the trend seen in past surveys that had indicated consistent growth of this workforce, with, for instance, the number of people active on the leading platform having increased by one-fifth in the previous measurement.

HIGHLIGHTS

The total gig workforce has declined by 17.8 percent since the previous measurement, breaking the double-digit growth seen in the aftermath of the pandemic.

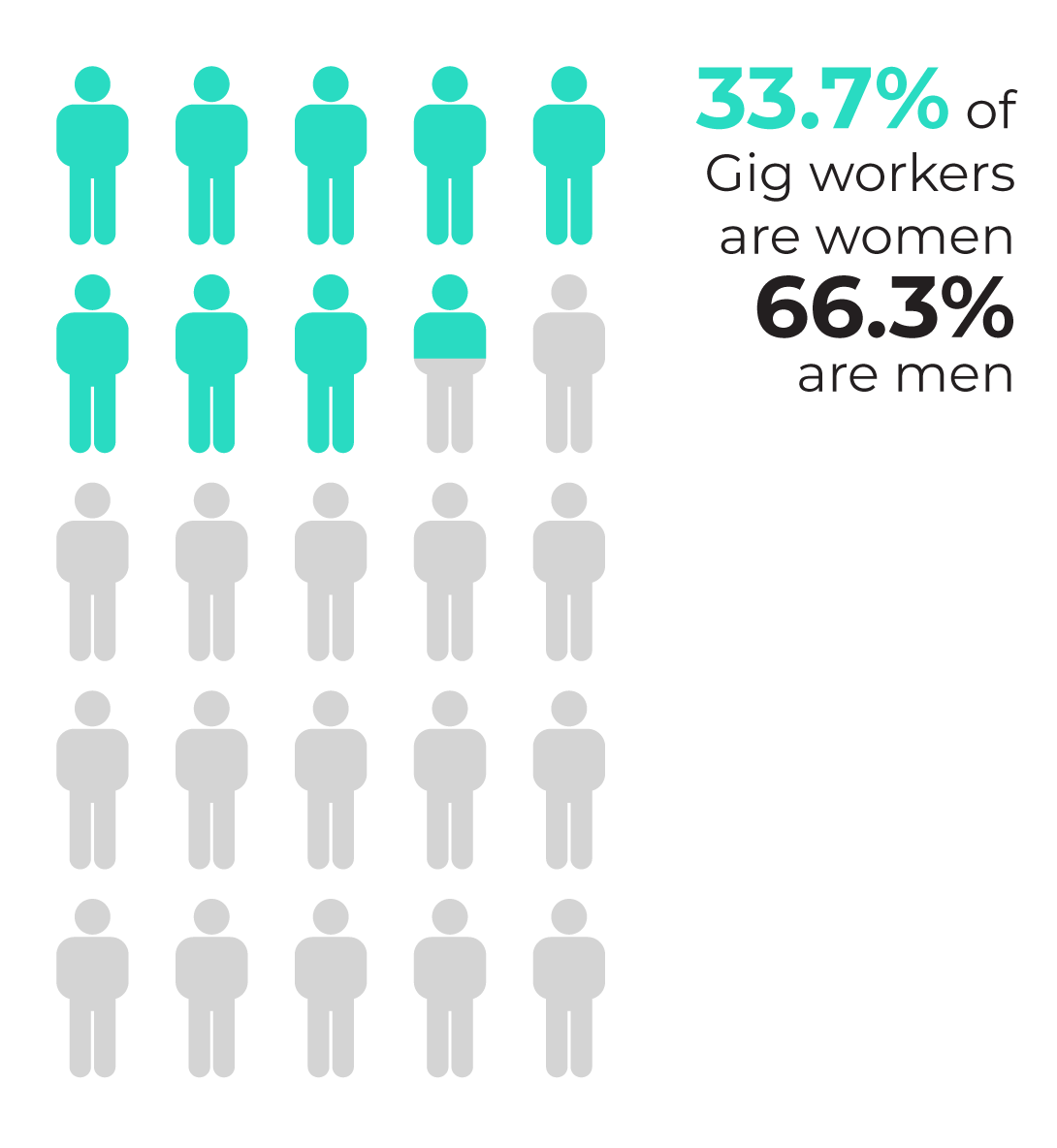

With most of those leaving the market being men, the share of women in the overall workforce has seen a slight increase of 1pp to 33.7 percent.

Writing and translation has registered the largest drop, especially for men, as male gig workers leaving the market outnumbered women by a factor of 4.4.

Women gig workers in software dev and tech are the only group not to have seen a decline in numbers.

Šumadija and Western Serbia is the sole region that has not recorded a decline in software dev and tech gig workers.

The average hourly rate has continued to increase, reaching the historic high of US$21.8, as both men and women gig workers have been demanding 3 percent higher wages per hour than over the previous six months.

RESULTS IN DETAILS

Doubtlessly, factors specific to the digital labour market have played a major role in this change. According to the latest research (Hui et al., 2023), the emergence of AI tools such as Chat GPT has significantly shaken the freelancing market, leading to a statistically significant decline in their jobs and income. As further indicated by this year’s Payoneer report, Serbian gig workers have been facing a surge in global competition, having trouble finding new work, and struggling with slower demand growth when compared to their global peers.

The shift could also be attributed to the absence of price competitiveness in certain occupations or a deficiency in knowledge and skills among Serbian gig workers. These factors collectively exert pressure on their position, earnings, and ability to secure work in the digital market. One should also not ignore internal developments in Serbia, in particular tax policy changes that have made it easier for freelancers to declare platform income whilst also imposing stricter controls on unreported earnings.

With that in mind, a large number of gig workers identified in the previous measurement as being prepared to move to traditional, non-platform employment arrangements seems to have done just that. In fact, in the latest survey, no more than 8 percent of all freelancers claimed they were ready to sign traditional employment agreements. This figure is significantly lower than the 27 percent seen in the previous survey, a development suggesting many have since acted on their intentions, leaving the market mainly to those seeking more flexible working arrangements.

Two things matter for the transition from platform to traditional work. One is that these are almost exclusively platform workers with considerable work experience, and the other that these freelancers command hourly rates nearly 30 percent higher than the Serbian gig worker average. These facts suggest that conventional employment agreements are particularly attractive for a substantial portion of the well-established freelancer workforce and that it seems obvious that the advantages of gig work are offset by drawbacks that have motivated this population to seek jobs that formally entail a different balance of rights and obligations between workers and employers.

% OF GIG WORKERS BY ADMINISTRATIVE DISTRICT

Continuous monitoring of the gig workforce by region has revealed most of these freelancers (84.1 percent) live and work in 28 Serbian cities and towns. The latest trends reveal a slight increase in their urban population, bearing out recent studies that have shown increasing spatial agglomeration of online freelancers.

The major drop in the national gig workforce is reflected in nearly all urban centres (24 of the 28). However, the decline has not been well balanced, with some cities registering a relative increase (in the size of the gig workforce relative to the total population), with others seeing a decline in this relative share. Interestingly, both relative decline and relative growth were recorded in an identical number of cities (14). By contrast, four cities, Jagodina, Užice, Kikinda, and Zaječar proved exceptions where gig workforces rose slightly. However, these locations all had rather small freelancer populations, ranging from 0.9 percent of the total in Jagodina to just 0.5 percent in Zaječar.

Administrative centres at the NUTS2 region level also returned mixed results. Here, Belgrade and Niš registered slight decreases in freelancer populations, with major drops seen in Novi Sad and, to a somewhat lesser extent, Kragujevac as well. This has led to Belgrade accounting for 41.2 percent of the total gig workforce in the latest measurement, followed by Novi Sad at 13.1 percent, Niš at 8.3 percent, and Kragujevac at 2.9 percent.

In the latest survey, ten cities had freelancer populations exceeding 1 percent, namely Subotica, Pančevo, Kraljevo, Zrenjanin, Čačak, and Kruševac. Leskovac has now dropped off the list, leaving Niš as the only city with a sizeable gig workforce in Southern and Eastern Serbia.

Regionally, the freelancer population saw its relative share increase significantly in Belgrade and, to a much lesser extent, in Šumadija and Western Serbia. Conversely, the remaining two regions, Vojvodina and Southern and Eastern Serbia, have registered large-scale contractions in their gig workforces.

Men seemed readier than women to leave the platform labour market over the past six months, as, regionally, the contraction in women freelancers was not as large as for their male counterparts. Consequently, the share of women has risen across all regions: less so in Belgrade and Šumadija and Western Serbia, and somewhat more markedly in Vojvodina and Southern and Eastern Serbia.

GIG WORKERS BY OCCUPATION

.

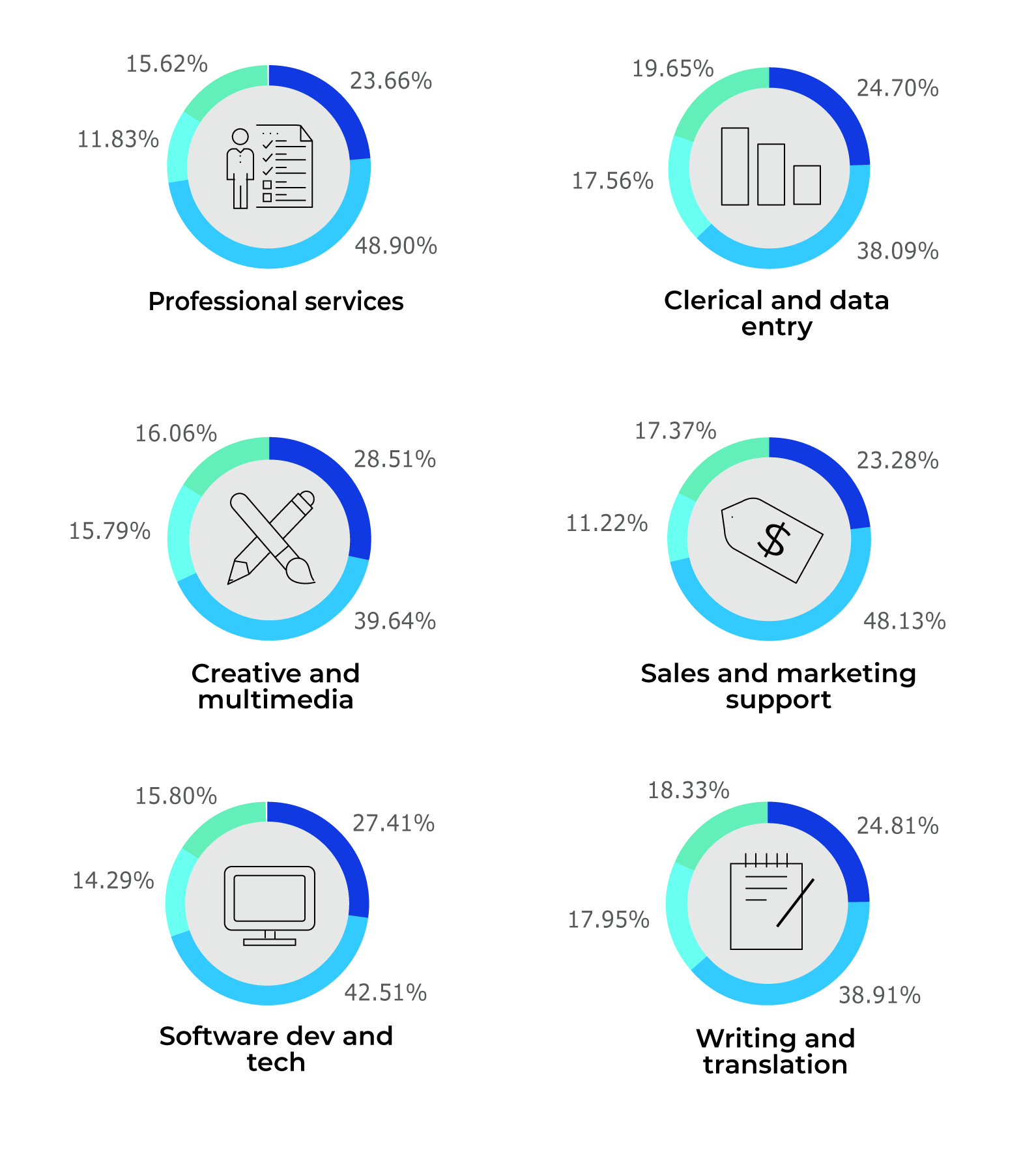

The charts in this report show the distribution of gig workers by occupation according to the Online Labour Index (OLI) taxonomy developed by the Oxford Internet Institute. The main finding of the latest measurement is the decline in freelancer numbers. This was the least pronounced in software dev and tech (at 2.4 percent) and much higher in professional services (13 percent). All other occupations registered decreases greater than 20 percent, with writing and translation seeing the highest fall at 28.7 percent. Apart from the increasing use of artificial intelligence for this work, one potential explanation for the large drop-off in writing and translation is the accelerating transition of freelance linguists to specialised platforms, although Upwork has remained one of the best digital marketplaces for people in this occupation.

Differences in the extent of the decline for each occupation have been reflected in changes to the relative shares of individual occupations in the total gig workforce. Creative and multimedia has remained the dominant occupation, accounting for more than one-third of the gig workforce (33.8 percent), even though its share in the total has continued to contract, declining by 1.4pp relative to the previous survey.

Only two occupations have managed to increase their shares, with professional services edging upward by 0.4pp and software dev and tech growing by a more substantial 4.2pp. Conversely, sales and marketing support has seen the lowest decline, at just 0.1pp, with clerical and data entry, creative and multimedia, and writing and translation all falling by a similar 1.5pp on average.

The key conclusion to be drawn from these trends is that occupations offering the highest incomes have proven to be the most resilient amidst the large-scale contraction. This finding accords with conventional economic theory, which says that the extent of the economic incentives determines the scale of labour supply in a market. An additional interpretation is that satisfactory conditions on demand side for software dev and tech or professional services and lower (global) competition faced by Serbian gig workers means fewer freelancers have chosen to leave the market. At any rate, this shift to better-paid occupations represents a major qualitative restructuring of the gig labour market.

REGIONAL GIG WORKERS AS % OF TOTAL, BY OCCUPATION

Whereas measurements to date have looked at the implications of market growth as reflected in the increase in regional freelancer workforces, the latest survey focused on the effects of market contraction on individual occupations across regions. Here, the latest measurement has allowed the researchers to test the hypothesis of evolutionary development and small-scale changes, an assumption proven in successive surveys during periods of growth, as well as to investigate the character and extent of these changes at times of market contraction.

The relatively large-scale drop in the professional services workforce in Belgrade (at 24.4 percent) has led to a 1.5pp decline in the share of Belgrade’s gig workers in this occupation. At the same time, the shares of gig workers based in the remaining three regions have grown, albeit only slightly so in Southern and Eastern Serbia and Šumadija and Western Serbia, with a more marked increase evident in Vojvodina (at 1.2pp). Read more ...

This was the sole occupation where the relative percentage of freelancers residing in Belgrade has declined, with their share growing across all other occupations, primarily in sales and marketing support (3.6pp) and slightly less so in software dev and tech (1.6pp), with a negligible increase reported for the remaining three occupations.

In Vojvodina, the relative share of gig workers has gone down by more than 1pp in no fewer than four occupations, namely clerical and data entry, sales and marketing support, software dev and tech, and writing and translation. Apart from an increase in the relative share of freelancers in professional services, moderate growth was also recorded in Vojvodina in creative and multimedia. This greater emphasis on relatively better paid work again constitutes a qualitative shift in the structure of Vojvodina’s digital labour market.

The features of the decline were different in Southern and Eastern Serbia, where less well paid occupations came to the fore. In this region, the relative shares of gig workers fell in creative and multimedia and software dev and tech, with an increase in freelancer populations recorded in the remaining four occupations, most notably writing and translation (at 1.1pp).

The shift in Šumadija and Western Serbia followed a pattern similar to that of Vojvodina, with gig workforces registering growth in the better-paid occupations of professional services, creative and multimedia, and software dev and tech, and contractions seen in the remaining three occupations, as sales and marketing support fell the most steeply (at 2.7pp).

% OF REGIONAL GIG WORKERS BY OCCUPATION

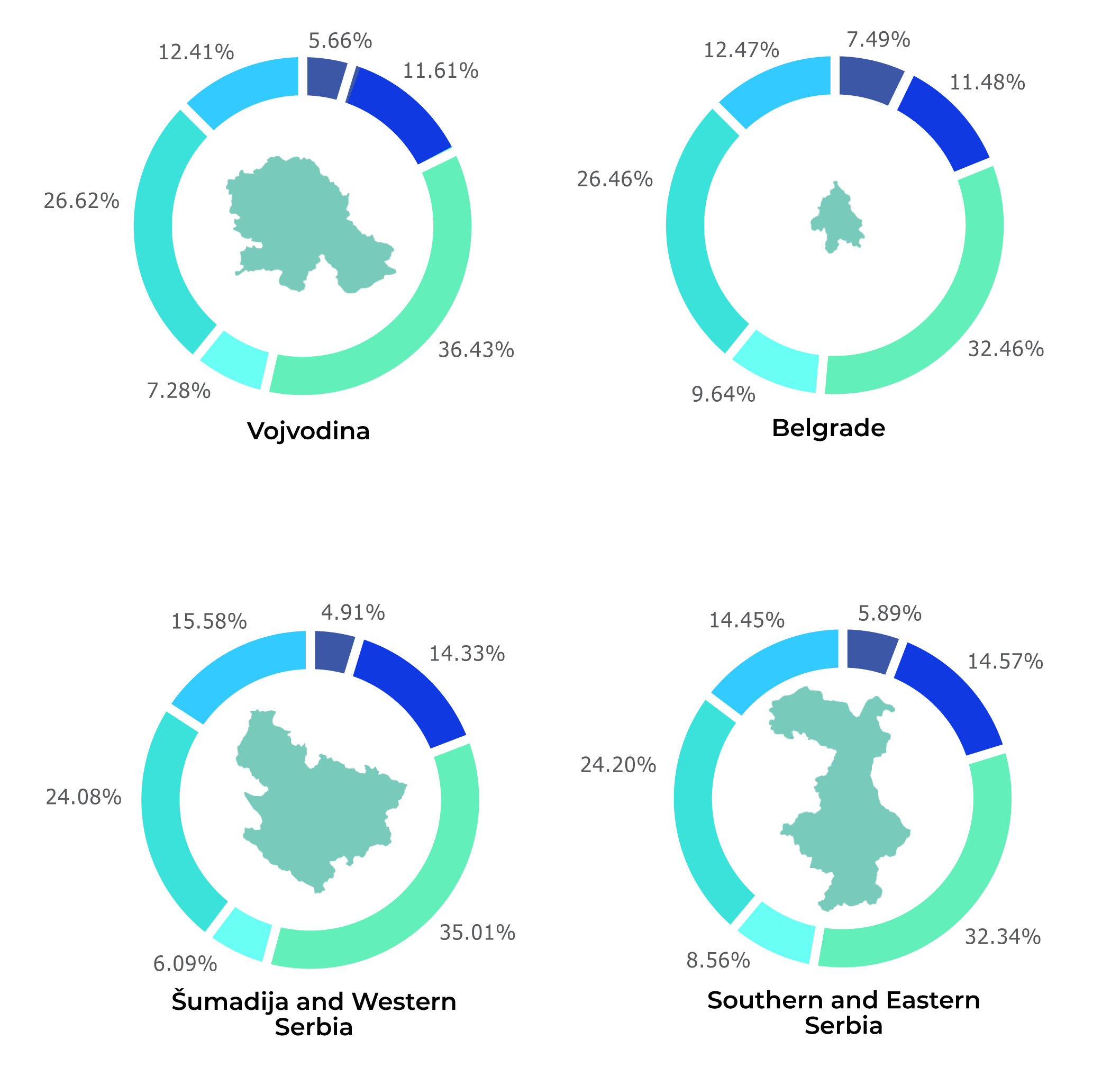

The decline of the overall freelancer population has also caused changes, albeit fairly minor ones, in how common particular occupations were in each region. Here, creative and multimedia (in first place) and software dev and tech (ranked second) have remained the most common occupations across all regions, with sales and marketing support (fifth place) and professional services (sixth) the least numerous ones. The sole significant change was seen in Southern and Eastern Serbia, where the large-scale decline in writing and translation freelancers caused this occupation to slide from third into fourth place, propelling clerical and data entry into its erstwhile third position. In other regions, clerical and data entry has remained third in size, followed by writing and translation. This has been a reflection of the local character of the contraction in Southern and Eastern Serbia, as well as of the fact that regional changes within each occupation were not sufficient to cause major shifts. The following sections outline trends common to all regions and identify areas that exhibited local differences relative to the previous measurement. Read more ...

The share of freelancers in professional services has grown relative to the total gig workforce in all regions, most markedly in Vojvodina, albeit even this part of the country recorded modest growth (of 0.7pp). Software dev and tech was the only occupation that registered the same trend across all regions, notwithstanding significant local differences: it grew the least in Southern and Eastern Serbia and Vojvodina (at 3.2pp), much more so in Belgrade (4.6pp), and saw the most pronounced increase in Šumadija and Western Serbia (at 5.4pp). Increases in the shares of the two best-paid occupations, software dev and tech and professional services, speak to the two major features of Serbia’s digital labour market. Firstly, there has been a shift towards occupations that are in high global demand, which has had the knock-on effect of enhancing the resilience of the online labour market. Secondly, economic incentives (in other words, earnings) are the key factor in explaining trends in the digital market, as the smallest demand-side contractions were seen in the best-paid occupations. Writing and translation was the sole segment that witnessed a drop in the share of freelancers in the total population, although this decline was less pronounced in Southern and Eastern Serbia at 0.8pp whilst standing at 2.2pp on average in the remaining three regions. Clerical and data entry saw a similar pattern, with only Southern and Eastern Serbia registering an unchanged share whilst the other parts of the country witnessed a moderate decline of 1.3pp on average.

A look at trends in the final two occupations, creative and multimedia and sales and marketing support, reveals some regional differences. Vojvodina has seen a slight increase in the share of gig workers in creative and multimedia, whilst the other three regions witnessed a decline in the relative importance of this occupation. By contrast, Belgrade and Southern and Eastern Serbia registered a slight increase in the relative significance of sales and marketing support, whilst Vojvodina, and in particular Šumadija and Western Serbia, saw a relative decline in gig workers engaged in this occupation.

The discrepancy between the most numerous occupation (creative and multimedia) and the least numerous one (professional services) has remained substantial, with the former outnumbering the latter by a factor of 5.3, but the gap has significantly narrowed since the previous measurement. The differences have been reduced across all regions, although they continue to be notable in Vojvodina (at 6.4) and in particular Šumadija and Western Serbia (7.1). This finding speaks to the emergence of greater balance in the structure of Serbia’s digital labour market, a development important for its future sustainability and stability.

GIG WORKERS BY GENDER

The latest measurement has revealed a continuing albeit slight (1pp) increase in women’s participation in the gig workforce, to 33.7 percent. Although this figure is much higher than in some other parts of the world, such as Asia (25 percent) or Africa (24 percent), Serbia is still lagging behind the averages for South-Eastern Europe (of 43 percent) and, especially, North America (50 percent).

The aforementioned contraction of the market has resulted in some changes to the gender structure of freelancers with experience of platform work and those with no such prior experience. Here, women workers with experience of platform work slightly outnumbered those with no such experience, with the situation identical for their male peers. For every 1,000 women gig workers with no income generated in the reporting period there were 1,121 who did earn some income, whilst for men freelancers the ratio was 1,000 to 1,107. This is a major change relative to the previous reporting period, when there were 1,300 women freelancers with at least some income for every 1,000 who had not earned income from platform work. What does this development suggest? The greatest number of women gig workers who have left the freelance market did have some prior experience, which may mean these women found the work less attractive or no longer suited to their needs. The reasons could include working conditions and arrangements that were relatively unattractive compared to the traditional labour market, including social insurance and taxation issues. The ratio of men freelancers with experience to those without it has remained substantially similar, suggesting that the shrinking market has affected both these categories equally, with both recent entrants and those with prior experience leaving the platform work arena. Moreover, the balance between the two groups testifies to the youth-centric nature of the digital labour market, with many seeking to try their hand at this type of work. Read more ...

The flight from the digital labour market has not affected all regions equally. Southern and Eastern Serbia and Vojvodina have seen far more men leave platform work than the remaining two regions, where the withdrawal was rather more balanced across both genders, even though men somewhat outnumbered women. This is borne out by the fact that the two largest individual contractions involving men occurred in Southern and Eastern Serbia (at -22.1 percent) and Vojvodina (-21.5 percent). Women withdrew from the gig workforce in substantial numbers in Šumadija and Western Serbia (with a reduction of -16.8 percent), but the remaining three regions saw fairly similar rates of downturn for an average of -15.6 percent.

% OF GIG WORKERS BY GENDER AND OCCUPATION

The general diminution of the gig labour market is also borne out by the reduction in in freelancer numbers regardless of their gender and occupation. However, even though the decline was universal, its pace was not, and this had an impact on the structure of the digital labour market, as well as on both occupations and gender balance.

The findings suggest occupations can be divided into three groups based on their rates of workforce flight. In the first group, characterised by the loss of more than one-quarter or one-fifth of the freelancer population, were writing and translation (which suffered the largest fall, at -28.7 percent), followed by clerical and data entry (-24.6 percent), and, lastly, creative and multimedia (-21.5 percent). The second category comprised sales and marketing support and professional services, where the contraction was less pronounced and stood at 19.6 and 13 percent, respectively. The third group was comprised of the most resistant occupation, software dev and tech, which fell by no more than 2.4 percent. Freelance work was evidently the most attractive option for tech professionals, which corresponds to the findings of recent research according to which developer jobs were the best rated freelance positions for pay, workload (‘hustle’), stability, and competitiveness. Moreover, instability in the tech industry, accompanied by layoffs, may go some way towards explaining why freelancers in this occupation were less likely to leave the digital labour market. Read more ...

The contraction at the occupation level was also visible when gender was taken into consideration. Writing and translation registered the greatest discrepancy, with men leaving the occupation outnumbering women who did so by a factor of 4.4. Expressed in percentages, the number of women active in writing and translation fell by 13 percent, with the male workforce in this occupation shrinking by 39.6 percent. Not only did writing and translation register the greatest contraction, but the change was the least gender balanced (tilted as it was in favour of women). Moreover, only clerical and data entry saw a reduction in women gig workers greater than 20 percent, whilst for men this was the case with no fewer than four occupations, with the two exceptions being software dev and tech (at 2.8 percent) and professional services (12.7 percent).

Professional services were the only freelance occupation left by fewer women than men, although the difference was modest at 13.3 vs 12.7 percent, respectively. In addition, the number of women freelancers remained virtually the same in software dev and tech (edging down by 0.2 percent).

Interestingly, changes in the Serbian digital labour market were at odds with global trends, at least when it came to demand for platform work in some occupations. For instance, a substantial number of both men and women left sales and marketing support, whereas globally marketing accounted for no fewer than 32.8 percent of all projects posted.

The varying paces at which the market shrank for the two genders has had a significant impact on the dominance of men in some occupations. Here, unlike in the previous measurement, where men outnumbered women in all occupations, in the latest survey women have taken the upper hand in clerical and data entry and writing and translation, even though the differences are not major. Besides, men were somewhat more numerous in professional services, outnumbering women by not more than 8.1 percent. Nevertheless, given the relatively limited workforce in this occupation, women are likely to become more numerous as early as by the time of the next measurement. By contrast, differences in other areas ranged from relatively moderate, such as in sales and marketing support, where men outnumbered women by a factor of 1.5, and creative and multimedia, where the figure was 2.1, to the massive discrepancy in software dev and tech, where for every 100 women freelancers there were 642 men. Nevertheless, despite these significant variations, the greater representation of women in all occupations is evident.

TOTAL INCOME BY GENDER

Freelancer income was determined by the interplay of five factors: the large preponderance of men over women freelancers, greater concentration of men in better paid occupations, men’s greater average income, greater inclination of women to treat gig work as a secondary source of income, and, lastly, greater than average engagement rate of women, a factor that works in the opposite direction from the remaining four.

The latest measurement has seen the continuation of a long-standing downward trend in the share of women’s gig work earnings in total freelancer income, with the reduction this year amounting to nearly 1.5pp. Amongst the many potential reasons for this the most significant ones are the general preponderance of men freelancers, greater concentration of men in better paid occupations, and the large discrepancies between men and women in the upper parts of the distribution (meaning amongst the best paid freelancers).

HOURLY RATES, IN US$, BY GENDER AND OCCUPATION

One especially interesting finding in the latest measurement is the major contraction observed in the number of gig workers notwithstanding the increase in their incomes. The hourly rates quoted by freelancers on their platform profiles have, on average, increased by 3 percent relative to the previous six months. This is the fourth consecutive survey to show income growth, with the average hourly rate for Serbian gig workers standing at its historic high of US$21.8. A mix of exogenous factors, such as inflation, and internal ones, including personal traits and the likely greater experience and skills possessed by gig workers who have remained active in the platform work market, has brought about the admittedly slight increase in the price of gig work. This represents a fundamental change, as the average asking hourly rate for Serbian gig workers has for the first time exceeded the global average of US$21 as reported for 2023. Nevertheless, Serbia is still lagging far behind the US, the world’s most highly developed digital labour market, as Serbian freelancers are now able to command only 40.5 percent of the average hourly rate earned by American gig workers.

Asking hourly rates have increased for both genders, although growth was slightly higher for women (3.2 percent) than for men (2.9 percent). The limited scale of these differences is best illustrated by the finding that women freelancers were able to earn 86.3 percent of their male peers’ hourly rates, a figure nearly unchanged from the previous measurement. This, however, confirms the conclusion of the previous survey about the fairly high persistence of gender-based income differences, which are, nonetheless, lower than those identified in other research, such as the 2023 Payoneer study, which found women freelancers could earn 81.8 percent of what their male counterparts made.Read more ...

The occupations can be divided into two groups by whether hourly rates in them grew or contracted. The growth group comprises sales and marketing support (with an increase of 6,2 percent), creative and multimedia (4.6 percent), professional services (5 percent) and writing and translation (0.6%), whereas the contraction group was made up of the remaining occupations, namely data entry and administrative services (-1.9 percent) and software dev and tech (-0.6 percent). The increasing hourly rates allowed platform workers to substantially augment their earnings. For instance, a Serbian freelancer working full time (176 hours per month) in sales and marketing support or creative and multimedia could earn an additional US$171.5 or US$145.1 every month compared to six months previously. These upward trends, especially in sales and marketing support, reflect growing global demand for gig work that has been particularly pronounced in the marketing sector. On the other hand, it is interesting to note that, despite the decline in average hourly rates in this occupation, freelance work has remained fairly attractive for Serbian IT professionals, as evidenced by the relatively limited contraction of this workforce. This continued appeal can be explained by the interplay of a series of factors, including the lifestyles of those active in the occupation (with many working from home even when they have traditional employment agreements); relatively high incomes (as the average full-time pay in software dev and tech stands at more than US$4,500 and these jobs are the best paid of any in the digital market); and, lastly, in all likelihood also by the nature of the work involved (with gig employment being a source of additional income for a large proportion of both men and women freelancers).

And, whilst a variety of trends were in evidence across occupations, the differences between genders were even more pronounced. Men were far more affected by adverse trends, as evidenced by the fact that male freelancers saw their earnings fall in four occupations, whilst women were similarly impacted in only one area. The decline in men’s incomes was particularly apparent in clerical and data entry (-6.9 percent) and writing and translation (-3.6 percent), with a minor contraction observed in professional services (-1.2 percent), whilst hourly rates in software dev and tech remained virtually unchanged (-0.1 percent). Although women freelancers saw incomes fall only in software dev and tech, the decline was quite pronounced (at -7.1 percent). Across the remaining five occupations, women gig workers registered the greatest increase in hourly rates in sales and marketing support (at 7.6 percent), which was also the highest growth rate of any gender or occupation. By contrast, men freelancing in creative and multimedia were able to earn on average 4.1 percent more than six months previously, making this the freelance occupation with the largest increase in income.

In the latest measurement, most Serbian gig workers, 3,555 in total, were found to have asking hourly rates of between US$3 (the lowest rate in this sample) and US$12 per hour. When added to the 2,733 freelancers asking for hourly rates of between US$12 and US$21, this figure means the majority of 62.5 percent of all gig workers commanded rates lower than the global average of US$21. Moreover, 25 percent of the gig workforce earned US$10 or less, whilst the second and third quartile earned between US$10 and US$30 per hour. By contrast, as few as 1.3 percent of the active freelancer population asked for hourly rates of US$100 or more.

_____________________________________________________

Recommended citation: Anđelković, B., Jakobi, T., Ivanović, V., Kalinić, Z. & Radonjić, Lj. (2023). Gigmetar Serbia, October 2023, Public Policy Research Center, http://gigmetar.publicpolicy.rs/en/serbia-2023-2/.

PREVIOUS REPORTS

HOW GIGMETAR WORKS

GigmetarTM is the first instrument that describes the geography of digital work in Serbia and the region in terms of gender, income, and most common occupations. It is a result of the efforts made by the Public Policy Research Centre (CENTAR) to shed more light on the work on online platforms.

ABOUT US

The Public Policy Research Centre (CENTAR) is a team of innovative researchers and digital enthusiasts investigating the future of work and development of the digital economy in Serbia and South-East Europe.

Contact: gigmetar@publicpolicy.rs