GIG WORKERS IN THE REGION

The latest regional issue of Gigmetar has identified a number of noteworthy trends: the labour supply has continued to contract, earning growth has been modest, and the gender gap has widened in terms of both labour market participation and earnings. These changes have been taking place in a sluggish global environment, with the World Bank forecasting growth of no more than 2.6 percent in 2024 and an average of 3.1 percent over a five-year period, the lowest rate in decades. In parallel with stable albeit slower growth, the global innovation environment has seen major changes, with the World Intellectual Property Office (WIPO) reporting a slowdown in research and development (R&D) spending, contracting investment, and a decline in scientific output. The World Economic Forum suggests multiple social, political, and economic factors have combined to produce a highly complex and largely uncertain business environment. Trends in the conventional labour market are especially significant, with employment in most South-Eastern European countries standing at a historic high and thus depressing labour supply in the digital market, even though flexibility and opportunities to earn more, gain experience and master new skills will remain incentives for workers to be active on digital work marketplaces in these economies. Not only does the combined impact of global and regional market trends and non-market-related factors explain the current contraction in the digital work market, but it also makes any future development highly questionable.Read more …

Apart from the broader economic environment, trends in the digital labour market will be shaped in equal measure by key technological advancements that have been having an increasing impact on how work is done. Applied artificial intelligence (AI), which seeks to automate, enhance, and accelerate processes is the principal factor shaping current – and, even more so, future – digital labour trends on both the demand and the supply side. Demand-side changes include fewer postings for repetitive and simple jobs, a trend identified by Gigmetar as the ongoing above-average decline in the demand for writing and translation and clerical and data entry work. By contrast, companies’ demand for digital skills has continued to increase, with AI use and development the most sought-after competencies.

The remote work revolution, which began with the COVID-19 pandemic, has persisted into 2024, with businesses continuing to enjoy the advantages of homeworking, especially the cost savings and access to a global pool of talent enabled by it.

Under these circumstances, how gig work will respond to the opportunities created by the global digital labour marketplace will largely depend on gig workers’ readiness and ability to upskill and reskill. The European Training Foundation has warned that any lack of adeptness at doing so may constitute a major obstacle to the future growth of the digital labour market in many South-Eastern European countries.

Freelancers have become a major part of the global workforce, with estimates putting their share in total worldwide employment at between 1 and 3 percent; moreover, a 2023 World Bank study suggests gig workers account for as much as 12 percent of the global labour force. As for 2024, the year can be neatly summed up in four words: more freelancers than ever. This tallies fully with the projected average annual growth of the digital labour market to 2030, which stands at 16.2 percent. These trends are particularly important for gig workers with technical knowledge and skills, as well as those active in marketing and professional services. Leading global firms have become increasingly dependent on gig workers: three out of ten Fortune Top 100 companies now employ freelancers, and Google has more freelancers on its staff than full-time employees. In India, one of the world’s fastest-growing and largest gig labour markets, 2024 figures show that nine out of every ten businesses have been considering hiring freelancers, with demand coming primarily from startups and the business process management sector. The growth in global demand for freelancers may seem to belie the Gigmetar findings of a contraction across the region’s digital work marketplaces, but the opening of new markets elsewhere in the world and entry of their workforces has greatly exceeded the decline in this part of the world, where it had been preceded by significant market saturation (in other words, a glut in supply), and which always accounted for a fairly minor share of the available global gig workers. Besides, there is no causal relationship between the abstract number of gig workers and their activity on digital platforms. In other words, freelancer numbers may increase, but this growth can be driven by their employment and flexible engagement by other means, such as through bilateral ad hoc working arrangements for clients away from platforms.

Gigmetar seeks to identify the general characteristics of the South-Eastern European (SEE) gig work market and the similarities and differences between countries in the region, as well as to identify key regional trends and ongoing changes. The latest measurement suggests the gig work market is being shaped by powerful forces, with the freelancer workforce registering the third consecutive contraction, and quite a substantial one at that.

HIGHLIGHTS

Continuing decline of the gig workforce. The latest measurement registered the third successive drop in the active gig workers on Southeast Europe’s leading digital platforms, amounting to 14.4 percent.

Upwork has remained the dominant platform, with Serbia still the largest national market. Upwork accounted for 57 percent of gig workers active on the three primary online work marketplaces, and Serbia was home to 25.6 percent of the region’s freelance workforce.

New entrants from the region’s EU member states have been finding it easier to get work. The average share of new entrants active at the time of the measurement stood at 32.1 percent in EU member states as opposed to no more than 25 percent in the other countries of the region.

Women left the digital work market in greater numbers. In the latest measurement, women gig workers made up 37 percent of the region’s gig worker population on average, with the percentages ranging from 46.5 percent in Albania to 30.6 percent in Bosnia and Herzegovina.

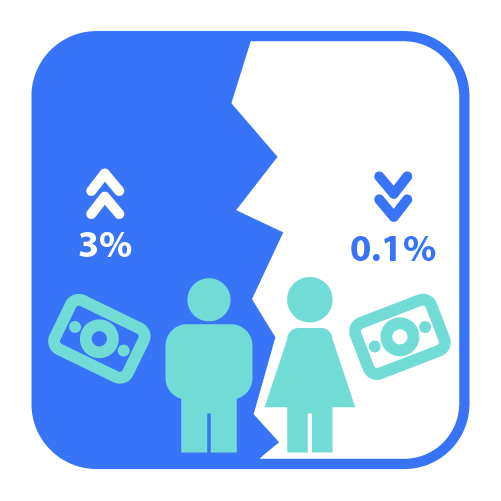

Quoted hourly rates[1] have been continuing to grow, albeit less quickly. Gig worker earnings have increased by an average of 3 percent relative to the previous survey. Women’s hourly rates, have, however, edged down (by 0.1 percent), in contrast to robust growth seen by their male peers (4.2 percent), widening the gender pay gap – with women now earning on average 83.4 percent of what men can make.

[1] ‘Hourly rates’, indicating the asking price of labour posted by gig workers on their online accounts, is used in Gigmetar interchangeably with ‘earnings’.

LEADING PLATFORMS

The latest measurement has identified the third consecutive fall in the number of gig workers active on major digital platforms across Southeast Europe (Upwork, Freelancer, and Guru). This contraction stood at 14.4 percent as against the 7.6 percent seen in the previous survey. As this measurement has registered the largest departure of freelancers from Upwork, its relative importance has declined, and it now accounts for 57 out of every 100 gig workers. Read more …

Digital platforms followed divergent trends. Freelancer and Upwork saw contractions in labour supply, whereas Guru saw negligible growth, at 1.1 percent on average. The drop was more pronounced on Upwork, where the freelancer workforce fell by nearly one-fifth (19.1 percent), whilst Freelancer similarly saw a slightly less marked decrease, at 16.1 percent. Although Upwork emerged the worst off in this measurement, seeing its share fall by slightly above 3.3 percentage points (pp), the platform still dominates the region’s digital labour market, accounting for 56.9 percent of all gig workers active across the three platforms included in the survey. Moreover, Upwork is by far the most dominant marketplace throughout the region, with its share ranging from 45.8 percent in Romania and 49.1 percent in Hungary to 68.9 percent in Albania and 69.4 percent in Montenegro. This finding is particularly telling in view of Upwork’s 2024 growth as measured by both the number of its clients (which increased by 2 percent) and improvement in its business indicators. One key factor in explaining this trend is that South-Eastern European workers are now becoming uncompetitive as their rates are significantly higher than those seen in other markets, especially South-Eastern Asia, as well as because freelancers now have a plethora of other alternative options at their disposal, both in the mainstream labour market or through various other remote working arrangements.

Evolving structure of the digital work market. The decline in Upwork’s share has been accompanied by changes to the relative positions of the other two platforms. The contraction in Upwork and Freelancer, and, to a lesser extent, its own growth, have combined to increase Guru’s share to nearly one-quarter of the regional workforce (24.6 percent). Freelancer’s contraction reduced its share to 18.5 percent of all freelancers across the region.

Uneven decline across the region. North Macedonia experienced the smallest contraction, with its freelance workforce declined by 9.9 percent, whilst, by contrast, Albania shed nearly one-quarter of its gig population, at 23.4 percent. The average fall for all other countries stood at 15.5 percent, although this may mask the variations identified in the measurement. Here, Serbia (at 11.6 percent), Romania (11.9 percent), and Bosnia and Herzegovina (13.7 percent) all saw moderate contractions, whilst Bulgaria (at 16.7 percent), Hungary (17.8 percent), and Croatia and Montenegro (both at 18.4 percent) registered more pronounced reductions.

Asymmetric workforce distributions by country. The latest changes, coupled with past trends, have meant nearly one-half of the region’s workforce is now concentrated in two countries, Romania (which is home to 24.2 percent) and Serbia (24.1 percent). Bulgaria is the sole country with anything approaching a greater share of the regional workforce (at 10.1 percent), whilst Montenegro, as expected given its size, accounted for the smallest proportion (2 percent). Bosnia and Herzegovina (6.6 percent) and Croatia (6.7 percent) also had some of the least numerous freelancer populations.

Limitations affecting outlook projections. Multiple factors may have affected the accuracy of these estimates. Firstly, there has been a change in the methodology of how gig workers are presented on the various platforms, and, with the procedure not publicly available, the different reports may not be directly comparable. Secondly, the same gig workers may have had multiple profiles on different platforms. The latter issue is not as significant since platforms have an interest in presenting only active workers available to potential employers and therefore update their gig worker databases fairly regularly. As such, even though some workers have profiles open on more than one platform, this does not affect estimates of the actually available workforce, since all those workers are active.

SHARE OF GIG WORKERS BY COUNTRY AS % OF REGIONAL TOTAL

Although Serbia lost 2,800 gig workers, the largest absolute number of any country, it is also home to more than one-quarter of the region’s freelancers. Croatia and Albania saw the greatest contractions, losing 25.6 percent of their gig worker populations over the last six months. Read more …

Large changes, but perspective matters: relative vs absolute declines in gig populations. Differences between regional countries were only those of scale, with two broad groups identified in the survey. Firstly, a set of countries saw a fairly modest but still notable contraction (at up to 20 percent) in their freelancer workforces: this group comprised North Macedonia (which registered the smallest decline, at 11.6 percent), Serbia (15.8 percent), Romania (16.2 percent), and Bosnia and Herzegovina (19.4 percent). The second group was made up of countries that shed more than one-fifth of their gig workers, with a fall of more than one-quarter see in no fewer than three of these, namely Croatia and Albania (25.6 percent each), as well as Hungary (25 percent). However, absolute numbers also need to be taken into account to completely understand the scale of these changes. For instance, even though Serbia shed 15.8 percent of its freelancers, the loss was far greater than in Croatia’s 26 percent decline, since the actual figure for Serbia was over 2,800 as opposed to less than half of this number, 1,230, who left the gig workforce in Croatia.

NUMBER OF GIG WORKERS PER 100,000 POPULATION, BY COUNTRY

For the first time since Gigmetar first started tracking trends in the major online work platforms, the number of gig workers has fallen to below 100,000 to stand at 90,204 active freelancers.

Given the size of the individual countries and the total regional population, relative changes were less pronounced. Despite the large drop in this indicator (191 freelancers per 100,000 population), Serbia has risen through the ranks into third place. North Macedonia has remained in pole position despite a major contraction in its freelancer workforce, having shed 37 gig workers per 100,000 population. The number of countries where this indicator is now below 100 has grown to four, with Croatia joining Bulgaria, Romania, and Hungary in this category.Read more …

The number of freelancers per 100,000 population has been in decline. Whilst in the previous measurement only three countries had fewer than 100 freelancers per 100,000 population (Bulgaria, Romania, and Hungary), this group has now grown to include Croatia, with 87 gig workers per 100,000 population. Hungary’s gig workforce has remained the smallest relative to its overall size, with no more than 37 freelancers per 100,000 population, the consequence of a 25-percent contraction.

North Macedonia and Montenegro: still the best but suffering a major decline. The top two countries by gig workers per 100,000 population were North Macedonia, with by far the largest freelancer population of 238 per 100,000 population, and Montenegro, where the figure was 202. These numbers were significantly lower than in the previous measurement, owing to a rather large fall in the indicator, with gig worker numbers per 100,000 population going down by 37 in North Macedonia and by as much as 57 in Montenegro. Albania fell from third into fourth place following its own large contraction, now seeing 187 freelancers to every 100,000 population.

REGIONAL GIG WORKERS BY PROFESSION

The latest labour market measurement has revealed a major contraction in the share of the digital workforce across all occupations. Professional services, writing and translation, and sales and marketing support were the hardest hit, having lost more than a quarter of their gig workers. Clerical and data entry also saw a significant downturn, at 22.7 percent, whilst software dev and tech (at 16.4 percent) and creative and multimedia (11.2 percent) were the least affected.

Freelancer workforces contracted at different rates by country, reflecting dissimilar structures of digital labour markets and disparities in workers’ abilities to adapt to global changes in demand for digital work. Read more …

Creative and multimedia and software dev and tech increased in importance at the expense of the other four occupations. The latest measurement has revealed some changes – albeit modest ones – in how gig workers are distributed by occupation. Increases in the relative share of two occupations in the overall freelancer population – a fairly large one (2.9pp) in creative and multimedia, and a relatively modest one for software dev and tech (0.9pp) – were accompanied by contractions across the other four occupations. Writing and translation saw the largest decline, of some 1.3pp, with smaller drops registered in professional services and sales and marketing support (at 0.9pp) and clerical and data entry (0.6pp). The declining share of writing and translation has been particularly important, not just as the most pronounced, but also because as it marks the continuation of a trend seen in the past four measurements. The automation of translation services has clearly led to many gig workers in this occupation leaving the market, with those who remain having to adapt by upskilling, mastering prompt engineering skills, and/or broadening their areas of expertise.

Large increase in activity rates. With more than 18,400 gig workers active at the time of the measurement, if Upwork, the region’s largest digital work marketplace, were a business, it would be the largest multinational corporation active across all of the countries surveyed. Here, in the previous measurement the number of gig workers active on the platform at the time had increased by as much as 53.3 percent, followed by an additional 50.1 percent increase in the latest survey. On average, these workers accounted for no less than 35.9 percent of the labour force, an increase in their share of more than 7pp over the preceding six months. In other words, more than one in three active gig workers registered on Upwork actually did work on a project at the time of the measurement. A key feature of the ongoing restructuring of the digital work market is the increasing number of freelancers who have the sufficient quantity of different knowledge and skills to find work, in parallel with the overall reduction in the total workforce. As such, the global digital work market – at least given the findings from the South-Eastern European countries surveyed by Gigmetar – is becoming increasingly professionalised, where those seeking to pursue careers as independent professionals gaining much more space to do so, whilst workers looking for additional (secondary) sources of income have been seeing much less scope for doing so.

Differences in activity between countries have remained substantial. The disparities identified in past measurements have remained significant, with two distinct groups of countries emerging. Countries in the first group have exceptionally active freelancer populations, with more than 40 percent of their total gig worker populations active at the time of the survey. This camp comprises only North Macedonia, whose workforce was the most active in the latest measurement (at 41.7 percent), and Serbia (where the share of active freelancers in the total stood at 41.6 percent). The second group is made up of countries where between 30 and 40 percent of all gig workers were active at the time of the survey and is headed by Montenegro (39.5 percent) and Bosnia and Herzegovina (37.7 percent), both with figures comparable to those seen in the last survey. European Union members constituted a separate sub-category here, with all seeing a decline in freelancer activity rates: Croatia could boast the most active gig worker population (at 34.6 percent), followed by Hungary (33.2 percent), Bulgaria (33.1 percent), and, lastly, Romania (31.7 percent). Albania was the sole exception to this downward trend: although no more than 26.1 percent of its registered freelancers were active on a particular project at the time of the measurement, this was nevertheless a huge improvement – of as much as 9.1pp – over the previous survey.

New entrants found it easier to get work, especially in the region’s EU members. Looking at national digital work markets from the perspective of first-time platform workers paints a different picture. For 27 out of every 100 freelancers active at the time of the survey, the project was their first job on the platform, an increase of 22.7 percent relative to the previous measurement. Here, the shares of new entrants were particularly large in Hungary (at 39.6 percent), Albania (35 percent), Romania (32.5 percent), and Bulgaria (31.3 percent). All other countries registered similar rates of new entrants that ranged from slightly above one-fifth to one-quarter of the total population. In this group, the proportion of first-time platform workers was the lowest in Serbia and North Macedonia (both at 21.4 percent), and the highest in Montenegro and Croatia (both at 25.1 percent). Also evident were differences between EU members and non-EU countries in this respect: whereas the average share of new entrants stood at 32.1 percent in the EU member states, the figure was as low as 25 percent in the non-EU countries. This disparity may be due to freelancers in EU member states possessing skills better aligned to global demand, as well as, to some extent, facing less competition in their chosen occupations (such as, for instance, Hungarian translators and content creators), making it easier for them to get work, including first-time jobs.

REGIONAL GIG WORKERS BY COUNTRY AND PROFESSION

The South-Eastern European digital work market exhibits major differences in contraction rates and sectoral specialisation. Whilst Croatia, Montenegro, and Hungary registered the largest fluctuations, Serbia and North Macedonia have shown resilience in some sectors, notably the information technology (IT) industry. The individual countries’ comparative advantages provide additional insights into the structure of the labour market. Here, Romania led the field in software dev and tech (which accounted for 29.8 percent of all gig workers), Montenegro was first for creative and multimedia (36.4), and North Macedonia was the leader in clerical and data entry. These trends reflect the impact of global demand for digital work, as well as country-specific factors, such as the availability of alternative work, the extent of digital skills, and economic stability. Read more …

Professional services, sales and marketing support, and writing and translation saw the largest contractions. Countries differed in the structure of their digital work markets by occupation. However, all countries shared the same downward trend relative to the previous measurement, with freelancer workforces declining in all sectors. Here, more than one-quarter of all gig workers left professional services (28.5 percent), writing and translation (26.3 percent), and sales and marketing support (22.7 percent). Clerical and data entry registered a slightly smaller drop (at 22.7 percent), whereas software dev and tech (16.4 percent) and creative and multimedia (11.2 percent) witnessed the smallest downturns. Potential explanations that may be key to understanding these trends include global demand for these services and the fact that little in the way of alternatives is available in the traditional labour market, especially in creative and multimedia, meaning platform work has remained the better alternative – and often perhaps the only one.

Professional services registered the steepest fall. National markets saw different occupations contract at dissimilar rates. For instance, professional services, the least numerous occupation, often registers the largest relative changes. In the latest measurement, for instance, professional services recorded a large-scale decline in Croatia (at 35 percent) even though no more than 113 workers actually left this occupation. Hungary saw the smallest contraction, with the workforce there falling by 16.3 percent. Writing and translation contracted the most in Albania (at 34.7 percent), Bulgaria (32.9 percent), and Bosnia and Herzegovina (30.5 percent), whilst, by contrast, the fewest workers left this occupation in Croatia and Montenegro, at 21.5 and 20.5 percent, respectively.

Sales and marketing support registered major differences by country. As many as 35.6 percent of all Serbian freelancers in this occupation left the digital work market, with similar findings also recorded in Albania, where the decline amounted to 31.4 percent. On the other end of the spectrum, Montenegro (at 13.2 percent) and North Macedonia (17.1 percent) registered far smaller but still significant contractions. Clerical and data entry was also hit hard by the departure of gig workers. This occupation also recorded significant disparities by country, although to somewhat lesser extent. Here, whilst Albania’s freelancer population declined by 30.1 percent, North Macedonian gig workers left the digital work market far less often, with no more than 11 out of every 100 choosing this option.

Contractions in software dev and tech differed the most between countries. Software dev and tech registered the broadest range of trends across countries. For instance, Croatia lost as much as 42.6 percent of its freelancers in this occupation relative to the previous measurement, although both Montenegro (at 35.2 percent) and Hungary (32.6 percent) also saw large contractions. Compared to these findings, the 4.1 percent drop in Serbia’s software dev and tech population, or the 5.3 percent decline registered in Macedonia, were both minimal. Not only were losses also generally smaller in creative and multimedia, but the differences between countries here were also much less pronounced: Serbia’s freelancers in this occupation were the least likely to abandon the digital work market (at 5.4 percent), whereas their Hungarian peers were the likeliest to do so, with 21.3 percent leaving the gig workforce over the past six months.

Country-specific changes driven by global factors. These findings, and the uniformity of the trends identified in the survey, suggest shifts in global demand are proving decisive for South-Eastern Europe’s digital work market. Nevertheless, a whole slew of country-specific factors – such as gig worker experience, alternatives available in the conventional labour market, and the sophistication of the freelancers’ knowledge and skills – have been crucial in determining the average ability of each country’s gig workers to survive in the highly competitive global platform work market during the past six months.

Comparative advantages of the countries in certain professions

A comparison of the relative share of an occupation in a particular country with its regional average can be used to identify the comparative advantages enjoyed by that country. The largest relative share of an occupation in a country suggests that country has an absolute comparative advantage in the regional context.

Despite Albania’s huge decline, which did, however, hit all occupations fairly equally, the country has continued to enjoy absolute comparative advantages in professional services and sales and marketing support. As in the previous measurement, North Macedonia has retained its absolute comparative advantages in clerical and data entry, as this occupation accounts for an even one-fifth of the country’s freelance workforce, whereas Montenegro has achieved a comparative advantage in creative and multimedia (with 36.4 percent of its gig workers active in this occupation). Romania enjoyed an absolute comparative advantage in software dev and tech, having widened its lead to see 29.8 percent of all freelancers active in this ear from the 28.7 percent registered in the previous measurement. Lastly, Hungarian freelancers were particularly specialised in writing and translation (18.7 percent) at the regional level.

Only one country, Romania, had as many as four relative comparative advantages, where an occupation had a larger share in the total freelancer population than the regional average for that occupation. This finding was at the same time a clear indication of how the structure of Romania’s digital work market differs from that of the region, as professional services, software dev and tech, and writing and translation – occupations where Romania enjoyed a relative advantage in the previous measurement – have now been joined by sales and marketing support.

As many as five countries registered comparative advantages in three occupations each. Here, Albania saw no change, having retained its advantage in professional services, clerical and data entry, and sales and marketing support. Hungary is the latest entrant in the three competitive advantages list and is unique in having an internal market that has undergone the most sweeping changes in terms of the structure of occupations. Here, apart from its traditional relatively large share of freelance writers and translators, the country has gained comparative advantages in professional services and clerical and data entry. Relative to the previous survey, Hungary has lost its advantage in software dev and tech. Bulgaria’s local digital work market is notable for its closeness to regional averages by occupation, but the country has nevertheless retained comparative advantages in professional services (which has now replaced creative and multimedia), sales and marketing support, and writing and translation.

Bosnia and Herzegovina also registered change, with the country again seeing comparative advantages in creative and multimedia and writing and translation whilst adding software dev and tech to the list. Montenegro enjoyed comparative advantages in the same occupations, together with writing and translation, which has emerged as a new focus area.

Three countries had comparative advantages in only two occupations, and in these the structure of occupations in the digital work market can be said to best reflect the regional landscape. One is Croatia, which enjoyed comparative advantages in sales and marketing support and writing and translation and has seen changes to its comparative advantages in every measurement to date, suggesting instability in the country’s labour supply. North Macedonia registered no change from the previous survey, and freelancers in this country continued to be relatively numerous in clerical and data entry and sales and marketing support. The absence of shifts in the North Macedonian market suggests the labour supply there remains the most stable with the clearest patterns of specialization. As in most of the region, Serbia witnessed changes, retaining a comparative advantage in creative and multimedia whilst gaining one in software dev and tech and losing one in clerical and data entry.

The far larger extent of change in comparative advantages by country registered in the latest measurement suggests that contraction has been driving restructuring across national gig work markets, with local and occupation-specific factors determining the final structure of each country’s freelance population.

REGIONAL GIG WORKERS BY GENDER

The previous six months were marked by the large-scale departure of women freelancers, and as their population contracted by 21.9 percent their share in the overall regional gig workforce declined to 37 percent. Montenegro and Albania witnessed particularly significant contractions in their women freelancer populations. Women were more numerous in professional services, clerical and data entry, and writing and translation, but the differences were minimal, especially in comparison with software dev and tech, where women were outnumbered by a factor of between 2.8 in Albania and 7.8 in Montenegro. Read more …

Gender gap has widened as women’s participation has decreased. The latest measurement has revealed a broader gender gap as the share of women in South-Eastern Europe’s freelance workforces has declined from 38.3 to 37 percent. However, although the decline in the relative importance of women gig workers was fairly minor, the latest findings suggest a shift in past long-term trends that had indicated larger or smaller growth in the share of women in the total freelancer population. This development was caused by the departure of more than one-fifth (21.9 percent) of the region’s women gig workers over the past six months accompanied by a somewhat less pronounced decline in the number of men (at 17.4 percent). Nevertheless, although South-Eastern Europe is lagging behind more mature digital work markets, such as North America, when it comes to gender equality, it is still far more egalitarian than most other countries or regions.

Montenegro and Albania have witnessed a major drop in the number of women gig workers in both absolute and relative terms. The region’s countries registered dissimilar trends in terms of gender structure. The rates at which men’s and women’s workforces shrank differed the most in Montenegro and Albania, in both absolute and, consequently, relative terms. Montenegro recorded a particularly large contraction, with women leaving the gig work market outnumbering men by a factor of 2.4, whilst in Albania the difference amounted to 1.4 times. The female gig worker population in Montenegro ultimately contracted by 35 percent, with the figure for Albania standing at 30.2 percent.

Greater, but not particularly severe, decline in women freelancers across the rest of the region. In Bosnia and Herzegovina, 20.3 percent of women and 19 percent of men freelancers left the platform work market; the figures for Croatia were 26 vs 25.3 percent, in Hungary 27.1 vs 23.9 percent, and in Romania 18.7 vs 14.8 percent. Serbia was the only country to register a more pronounced whilst still comparable difference, with the female workforce contracting by 20.4 percent as opposed to 13.3 percent for men. Lastly, men were more likely to abandon the gig work market in the remaining two countries, with the male workforce shrinking by 23.7 percent and the female by 21.6 percent in Bulgaria, and the figures standing at 12.3 percent for men and 10.6 percent for women in North Macedonia.

Women gig workers’ shares tallied with the absolute numbers. Most countries registered declining shares of women in the overall workforce, with the shift ranging from 7.4pp in Montenegro, the largest fall, to 0.2pp in Croatia, where the gender structure changed minimally. Women gained share relative to the previous measurement only in two countries, namely Bulgaria, where their participation rose to 39.5 percent (up by 0.7pp), and North Macedonia, with 41.1 percent (up by 0.5pp). And, whilst the Albanian market has remained the most egalitarian, with women accounting for 46.5 percent of the total, Bosnia and Herzegovina continued to record the lowest share of women in the gig workforce of 30.6 percent.

Despite the decline in their numbers, women are more numerous in writing and translation, professional services, and clerical and data entry. Changes to individual occupations have also been interesting to observe. Women have become more numerous in writing and translation, with an increase of 10.3 percent, and have retained their advantage in numbers in professional services (16.9 percent) and clerical and data entry (14.8 percent). Moreover, women have increased their lead on men by as much as 8.9pp in professional services and by 6.9pp in clerical and data entry. A look at these two occupations by country reveals interesting findings. Here, women lead men in Albania, Bulgaria, Croatia, Montenegro, North Macedonia, and Romania, but it is only in Albania, North Macedonia, and Romania that the difference is substantial, standing at 48.1, 46.5, and 30.8 percent, respectively. In the remaining countries the difference ranges from 18.6 percent in Croatia to no more than 3 percent in Montenegro, whilst Serbia’s gig workforce was evenly split between men and women. Moreover, women were less numerous than men in Hungary (by 25.3 percent) and Bosnia and Herzegovina (by 15.4 percent). The differences were even more pronounced in clerical and data entry, where, for instance, in Albania and Montenegro women outnumbered men by a significant 71.4 and 63.6 percent, respectively. The preponderance of women was less pronounced in other countries, and in Bosnia and Herzegovina and North Macedonia they were less numerous than men, by 25 and 8.3 percent, respectively.

Exceptions, however, do exist. Although in aggregate women freelancers were more numerous than men in writing and translation, findings by country were far more diverse. Women were more numerous by a wide margin in five countries (Albania, Croatia, Montenegro, North Macedonia, and Romania), with figures ranging from 44.4 percent in Albania to 14.5 percent in Croatia. By contrast, in the remaining four countries women accounted for the lesser part of the writing and translation workforce, with the difference ranging from 2.2 percent in Hungary to 6.9 percent in Serbia.

Where do men dominate, and is this dominance the same across all occupations? Men were more numerous in the remaining three occupations, but the extent of gender inequality differs markedly by occupation. The differences were fairly small in sales and marketing support, where men were more numerous by 20.9 percent at the regional level, more pronounced in creative and multimedia, where the figure was 85.6 percent, and exceptionally wide in software dev and tech, where men outnumbered women by a factor of 5.5. However, there was little to no change relative to the previous measurement, with only a minimal increase in favour of men in sales and marketing support and creative and multimedia. The most significant shift was registered in software dev and tech, where men had previously been more numerous than women by a factor of 3.6, and the figure has now increased to 5.5. These findings suggest that, as the market contracts, the population of women freelancers in software dev and tech has been exhibiting the greatest elasticity of labour supply.

Major differences between countries. The measurement has identified some differences between countries for these three occupations. North Macedonia registered a major increase, of 183.8 percent, in men freelancers in creative and multimedia, whilst the figures for Bosnia and Herzegovina and Hungary were 161.1 and 107.7 percent, respectively. The differences were less pronounced in sales and marketing support, ranging from 54.9 percent in Hungary to 10.4 percent in Montenegro. Interestingly, women outnumbered men in this occupation in Albania by as much as 59.4 percent, so providing the sole regional exception.

Large-scale changes have persisted and grown in software dev and tech. Software dev and tech was the sole occupation where the difference has remained highly pronounced, with men outnumbering women by a factor of 5.5. Here, the disparity was the smallest in Albania, where men outnumbered women by a factor of 2.8, whereas in three countries the gulf was similarly vast, with Montenegro seeing the greatest gender gap (7.8 times more men than women), followed by Serbia (7.5) and Croatia (7.4).

HOURLY RATES, IN US$

Average hourly rates saw a slight increase of 3 percent over the past six months. However, the differences between the countries were significant, ranging from a minor dip in Albania (at 0.2 percent) to robust growth in Croatia (6.1 percent). At the same time, Croatian freelancers’ hourly rates now top the list at US$26.9.

The 0.1 percent fall in women gig workers’ earnings, coupled with the 4.2 percent increase in men’s average incomes, has widened the gender pay gap, with women able to earn 83.4 percent of male freelancers’ average incomes. The gap has particularly broadened in Albania, Hungary, and Serbia, by more than 6pp on average, whilst Hungary was the sole country where women earned less than four-fifths of what men did.Read more …

The latest measurement registered a modest increase in earnings, although this was slightly higher than in the previous survey. At the regional level, incomes have grown by 3 percent on average, 1pp more than in the last measurement. Individual countries have, however, seen divergent developments. Here, the only country where average hourly rates edged down was Albania, which saw a 0.2 percent decline that continued a trend identified in the previous survey. Growth was also unequal, with Croatia (at 6.1 percent) and Serbia (5.9 percent) seeing the highest rates. Put differently, gig workers in these two countries could make on average US$1.5 and US$1.3 per hour more, respectively, than they had been able to six months previously. Nevertheless, both Bulgaria and Bosnia and Herzegovina also recorded above-average income growth, at 4.8 and 3.8 percent, respectively. Growth was far more modest in the remaining four countries, ranging from 0.2 percent in Montenegro and North Macedonia to 1.8 percent in Romania and 2.2 percent in Hungary.

Croatia registered the highest average hourly rates. Divergent income growth captured by the latest measurement has driven Croatia into first place by average hourly rates, up from third position in the previous survey. Bulgaria came second (up from fourth place), whilst Montenegro saw the largest drop in its hourly rates, falling into fourth place from its top position in the previous measurement. Although the region’s average hourly rate stood at above US$20, Macedonia provided the sole exception, with an average rate significantly below the regional average at US$18.3.

Women’s incomes have slumped to 83.4 percent of men’s. The latest measurement was characterised by diverging trends by gender. Whilst women’s average hourly rates saw a dip (at 0.1 percent), those of men have grown by a robust 4.2 percent. This has widened the gender income gap, with women able to earn on average 83.4 percent of what men could, in a major fall from the previous measurement (where the figure had been 87 percent). Nevertheless, even these findings notwithstanding, the region remains one of the most egalitarian globally.

Women’s hourly rates did not fall across the board. Moreover, whilst men’s hourly rates rose across the region without exception, those of women slumped in only three countries, Albania (4.8 percent), Hungary (3 percent), and Montenegro (2.6 percent), whilst Macedonia saw no change. By contrast, women’s incomes grew significantly in Croatia (by 5.6 percent), and Bulgaria (3 percent). Men’s hourly rates increased the most in Serbia (7.7 percent), Croatia (6.1 percent), and Bulgaria (5.9 percent), and the least in Montenegro (0.1 percent) and North Macedonia (0.4 percent).

The gender income gap widened throughout the region. For the first time, diverging trends and the pace of change in all countries have resulted in the income gap widening across the region, although countries differed by the extent of this effect. Specifically, the gender gap grew substantially in Albania, Hungary, and Serbia, by 7.4pp, 6pp, and 5.6pp, respectively. By contrast, at 0.3pp, Bosnia and Herzegovina registered minor changes, as did North Macedonia at 0.4pp and Croatia at 0.6pp. These trends have completely altered the regional gender income equality landscape. Albania slipped from first place into second, with women freelancers there able to earn 86.8 percent of what men are able to. Conversely, Bosnia and Herzegovina was the most egalitarian, as women in this country earned on average 87.1 percent of men’s average incomes, and this finding was all the more interesting since Bosnia and Herzegovina registered the lowest regional share of women in the gig workforce (of no more than 30.6 percent). Hungary and Serbia saw their relative positions worsen greatly, sliding into the last and penultimate position, respectively, for this indicator. Here, Serbia fell further, from fourth into next to last place, whereas Hungary slipped two positions down. Finally, Hungary was the only country where women could earn under four-fifths, or 79.7 percent, of what men were able to.

_____________________________________________________

Recommended citation: Anđelković, B., Jakobi, T., Ivanović, V., Kalinić, Z. & Radonjić, Lj. (2024). Gigmetar Region, October 2024, Public Policy Research Center, http://gigmetar.publicpolicy.rs/en/region-en-2024-2.

PREVIOUS REPORTS

HOW GIGMETAR WORKS

GigmetarTM is the first instrument that describes the geography of digital work in Serbia and the region in terms of gender, income, and most common occupations. It is a result of the efforts made by the Public Policy Research Centre (CENTAR) to shed more light on the work on online platforms.

ABOUT US

The Public Policy Research Centre (CENTAR) is a team of innovative researchers and digital enthusiasts investigating the future of work and development of the digital economy in Serbia and South-East Europe.

Contact: gigmetar@publicpolicy.rs